With a 38-year-history ranking residential real estate’s most successful U.S. brokerage firms, RISMedia’s annual Power Broker Report & Survey has had a front row seat to industry change, witnessing the various stages of the brokerage lifecycle—growth, acquisition, merger, rebrand, as well as shops closing up for good.

The degree and pace of change in the current residential brokerage landscape, however, is unprecedented. Not only is the process of transacting real estate fundamentally changing, so are the major players, so much so that by this time next year, the Power Broker Report stands to look diametrically different. And in subsequent years, permanently altered.

10 years of top 10

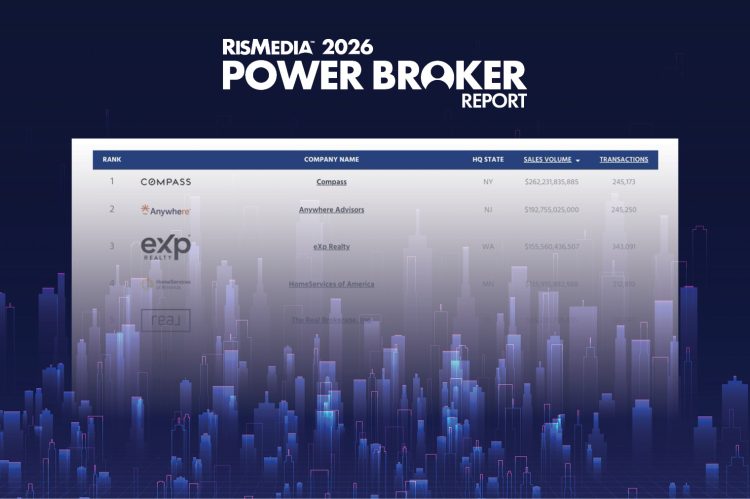

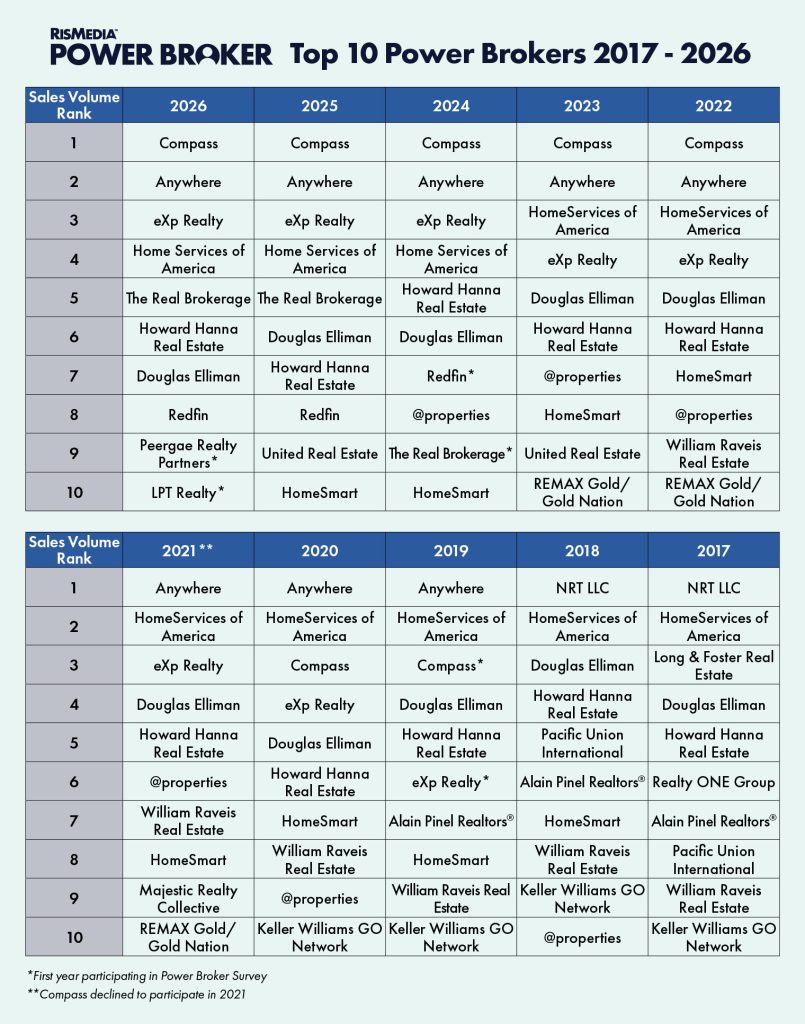

The Top 10 brokerages according to sales volume in RISMedia’s 2026 Power Broker Report remain largely unchanged from the previous five years. Aside from some jockeying up and down a rank or two, familiar players have held strong at the top of the chart.

Historically, the No.1 and 2 spots in the Power Broker ranking were dominated by Anywhere (previously NRT/Realogy) and HomeServices of America. Big change occurred in 2022, however, when Compass ascended to the No. 1 spot in sales volume just four years after its first appearance in the report at the No. 3 spot in 2019. Other shake-ups to the Top 10 over the past 10 years were the result of acquisition—such as when HomeServices of America acquired Long & Foster in 2017, and when Compass acquired Pacific Union and Alain Pinel in 2018 and 2019 respectively—and emerging models gaining strength, including eXp Realty, The Real Brokerage, Redfin and LPT Realty.

When reviewing the Top 10 of the past 10 years, it’s worth noting the speed in which new entrants to the market ascended to the upper echelon of the Power Broker ranking. Consider the founding dates of five of this year’s Top 10 brokerage firms to fully appreciate the rapidity of their growth:

eXp – 2009

United Real Estate – 2011

Compass – 2012

The Real Brokerage – 2014

LPT Realty – 2022

The changes we’ve seen thus far to the Top 10 Power Brokers will pale in comparison, however, to what’s on deck for next year when Compass will add a full year of Anywhere’s company-owned shops, as well as the firms recently acquired from No. 9 Peerage Realty, to its production data. Barring any additional earth-shattering mergers and acquisitions, Compass will put considerable distance between itself and the No. 2 spot, with a potential annual sales volume close to $500B and transactions north of 500,000, based on the 2025 reported data of Compass, Anywhere and Peerage.

A glimpse into what this might look like emerged during Compass’ Q1 earnings release: The company saw $2.7 billion in revenue, up about 59% from $1.7 billion in Q4 2025 and 99% from $1.36 billion in Q1 2025—an increase attributed to the addition of Anywhere brand’s revenue in the first quarter.

On the brokerage side, gross transaction value for Compass was $97.3 billion in Q1 2026, up 48% from $65.6 in Q4 2025 and 85.7% from $52.4 billion in Q1 2025. Compass agents closed 99,504 total transactions throughout the quarter, up from 60,328 last quarter and 49,121 last year. Increases were again attributed to the addition of Anywhere’s business to the Compass ecosystem.

A shifting franchise landscape

While the 2027 Power Broker Report will reflect this massive shift next year, big change is also on the horizon for franchise representation among the Top 1,000 firms included on the Power Broker ranking.

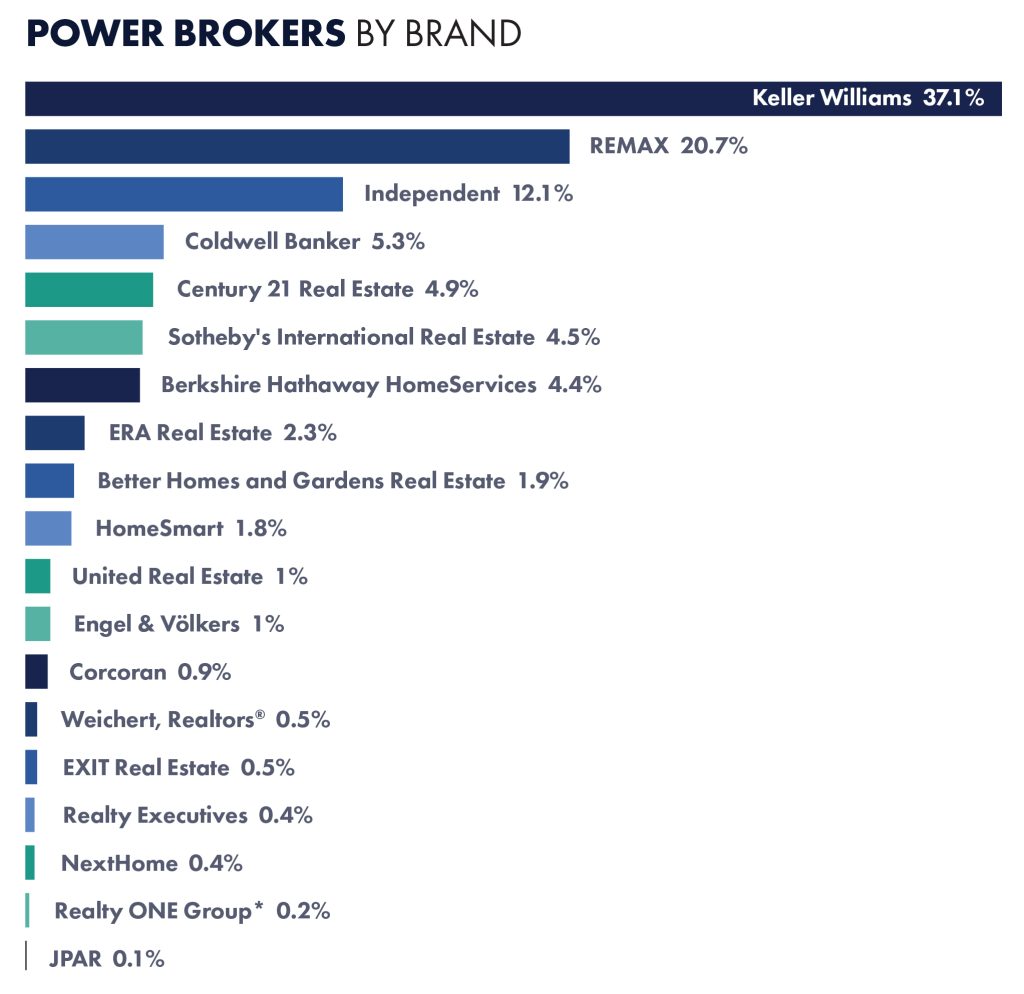

Historically, the No. 1 and No. 2 spots in terms of franchise representation have been securely held by Keller Williams and REMAX, with Keller Williams edging out REMAX this year with 37.1% of the Top 1,000 compared to REMAX’s 20.7%. The third-place spot for Power Brokers according to franchise affiliation goes to the independents, accounting for 12.1% of the Top 1,000 this year.

With The Real Brokerage’s recent acquisition of REMAX and eXp’s acquisition of NextHome, will the Power Broker by Brand statistics begin to change? While both organizations have initially said they plan to leave the franchising arms of the consolidated firms largely untouched, will we see representation decrease for REMAX, NextHome and the Anywhere brands as franchisees seek a new home or independence? Or will these franchisors become a more attractive opportunity to brokers with promises of a technology and resource infusion?

Or, will the corporate entities grow as franchisees facing renewal are absorbed by their new parent as we saw when many Berkshire Hathaway HomeServices firms migrated to company-owned shops?

For now, Compass, Real and eXp have promised to operate their company owned and franchise operations separately, infusing the latter with better tech systems and resources at some point.

During Real’s recent Q1 earnings call, CEO Tamir Poleg said, “We told them that nothing changes for now. It’s business as usual, obviously, but we also indicated that this combination will allow us to invest even more in growth, in technology, in strengthening the value proposition, both on the Real side or on the Real model and on the REMAX model.”

Similarly, eXp CEO Leo Pareja told investors during the firm’s Q1 earnings call, “There will be no changes to the NextHome brand. It is a different offering as a complete separate chassis.”

What will brokers do?

Another number to watch next year will be the percentage of independents in the Power Broker Top 1,000. In the face of consolidation, stories of brokerages opting out of Compass and returning to or launching independent models are already emerging. Next year’s Top 1,000 by brand affiliation may see lower numbers for Anywhere brands—Coldwell Banker, Century 21, ERA, BHGRE, Sotheby’s and Corcoran. The same may be true for REMAX and NextHome.

“Consolidation is likely to accelerate, and we’ve seen it first hand as a Corcoran affiliate—we are now part of Compass Holdings International,” commented David Howell, CEO of Corcoran McEnearney. “Yet we remain locally owned and operated and in control of our own policies and direction. To the extent that consolidation offers us more resources, that’s a positive. Consolidation that trends toward more brokerages ‘going their own way’ and diminishing the value of the MLS isn’t good for our industry.”

Individual brokerage firms trying to navigate the landscape have mixed reactions and concerns. In a recent interview with RISMedia, 27-year veteran Joseph Hamdan discussed his move from 18 years with Coldwell Banker to become the independent firm, MYNY, with four offices and 135 agents serving New York City, Long Island and the Hamptons.

“There were a few factors, but it ultimately came down to control and performance,” said Hamdan. “When there’s too much sameness across brands, it becomes difficult to truly differentiate, which puts agents at a disadvantage.

“We’ve never wanted our agents in a position where they can’t compete. Once we saw that clearly, the decision became straightforward. We now have the ability to grow the business on our terms, with every decision aligned around agent performance.”

Similarly, many existing independent brokerages believe the massive consolidation deals offer them a strategic advantage.

“Upheaval in the mega-consolidation realm is sometimes a threat and sometimes a blessing to mid-sized independents,” said Claudia Stallings, CEO of Wallace Real Estate. “We can retain our identity and provide familiarity to the consumer.”

Clint LaCour, CEO of New Orleans, Louisiana’s Reve | Realtors, agrees with Stalling and anticipates a larger move toward agent professionalism in the wake of consolidation—an advantage for those real estate professionals who remain a cut above the status quo.

“Consolidation and policy changes will accelerate the gap between high-service, professional operators and everyone else,” says LaCour. “In 2026, consumers will be more cost-aware and negotiation-driven, which favors experienced agents and strong local brands. Net: near-term friction, long-term positive for professionalism and market share.”

“Industry consolidation that accelerated in 2025 will benefit strong, well-capitalized brokerages and experienced agents in 2026,” said Jackie Viard, president of Signature Premier Properties on Long Island, New York. “While there will be fewer competitors, the overall professionalism of the market should improve, creating a positive impact on transaction quality and consumer experience.”

To see the Top 1,000 brokerage firms ranked by 2025 sales volume, please visit RISMedia’s 2026 Power Broker Directory.

{kind=link}