A transaction starts with a seller, and ends with a buyer. Everything in between is theoretically flexible—though for many years, not much has changed, as sellers have relied on agents to list properties directly on local MLSs, which subsequently syndicate properties to consumer portals that have the most reach with buyers.

Today, the industry faces a swift reordering of this process, centered on who makes the rules and who controls the data. Nearly every level of real estate—from the part-time agents to the super-sized portals—is likely to be impacted to a greater or less degree. While the “old” order appears largely intact still, the flow of listings (and the balance of power) has shifted considerably, as brokerages, MLSs, portals and vendors seek to expand or consolidate their control over listings.

What does that look like? The new processes are very much still in flux, with countless variations. But at the highest level, more and more listings appear to be taking new paths between buyer and seller, or skipping steps—opening up opportunities for the balance of power to shift, as listings give companies the power to influence policy or outgrow competitors.

While this picture is vastly simplified, and currently a huge majority of listings are still following the traditional path of MLS-to-everyone, a growing number of real estate leaders have made it clear they do not believe the old process will hold for the future.

The first movers

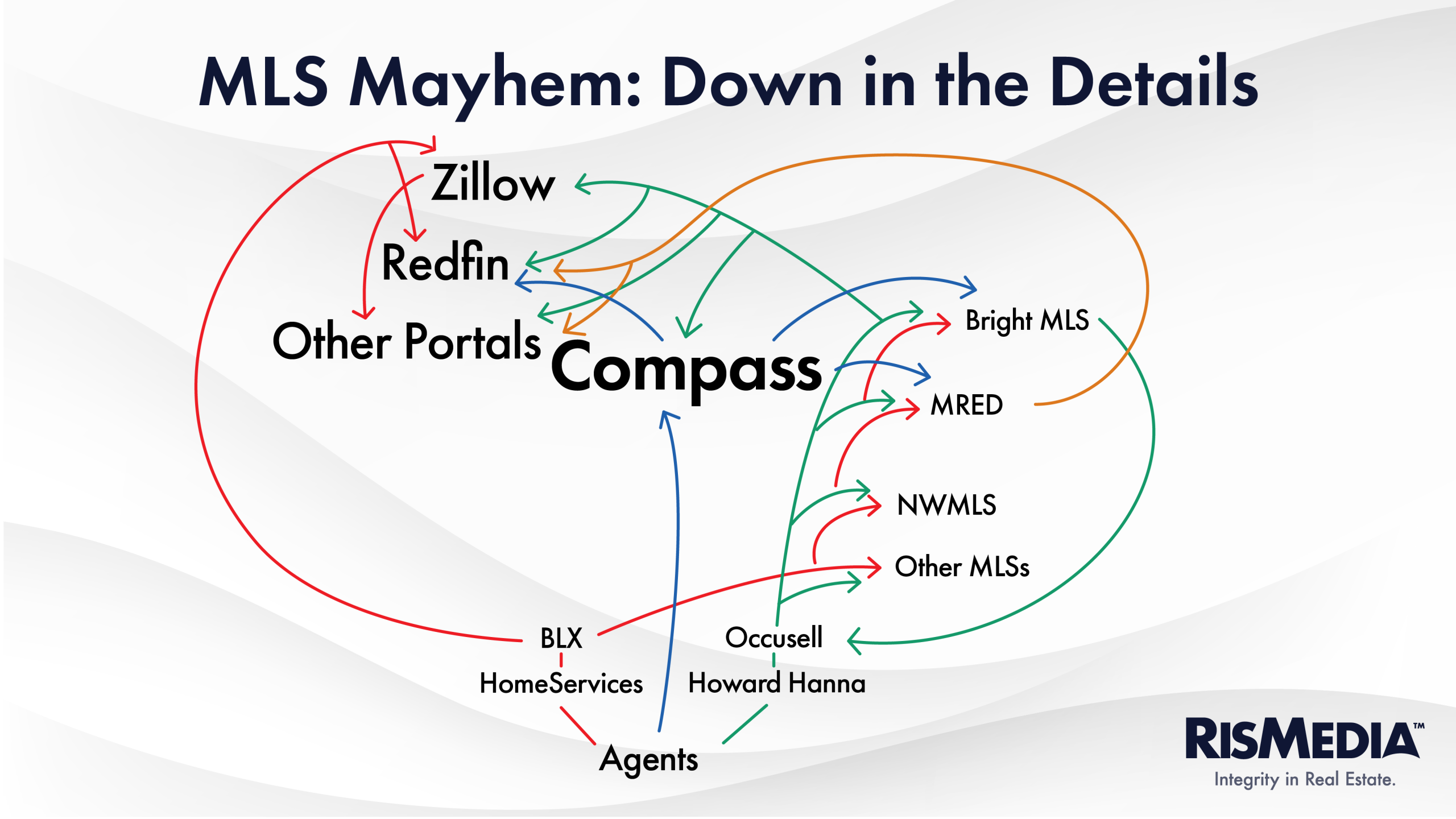

Compass has received the most attention for effectively kicking off the shake-up with a focus on its “Private Exclusives,” listings that initially are only hosted on its internal platform. Critics have accused the company of using this to double-end deals, but what it effectively means is that Compass controls a significant swath of inventory.

That power allowed Compass to lobby or pressure MLSs to shift their rules in ways that favor its marketing strategies, as well as strike a deal to share exclusive listings with Redfin, which catalyzed nearly every other large brokerage and portal to formulate similar pre-market programs.

Shifting the flow of listings to Compass’s own platform before going to the MLS (or Redfin) is something the brokerage has fought hard for (in the name of “seller choice”), and underscores the tremendous importance of who controls listings at every stage. Even though the vast majority of Compass’s exclusive listings eventually sell on the MLS, the brokerage has invested tremendously in being that first step, and effectively utilized this power to grow its business and influence policy.

Another aspect of listing control is the so-called third party “listing access platforms.” Real estate data giant Cotality earlier this year launched what it called the Broker Listing Exchange (BLX), meant to allow “listing data and distribution strategy from the moment a listing starts.” Howard Hanna announced that Ohio-based software company Ocusell would provide the brokerage’s internal listing platform, with the company already in a “joint venture” with Bright MLS.

While MLSs have long relied on outside software vendors for hosting or inputting listings, these partnerships have taken on new urgency and meaning this year. Cotality touts how the BLX allows “strategic distribution across the MLS, portals, and partners in full alignment with their specific policies and professional standards,” while Bright announced it is in discussion with an unspecified number of “large brokerages” to “consolidate their data” on Ocusell.

These platforms are not designed to “circumvent” the MLS, according to HomeServices President and CEO Chris Kelly, whose brokerage was one of the first to sign on to use BLX (along with Keller Williams). But Kelly also acknowledged that “recent industry developments” were part of the brokerage’s decision to use the platform.

“Brokerages have become increasingly dependent on a complex web of downstream data relationships to access and utilize their own aggregated listing information,” he wrote.

Effectively, though, brokerages that use these platforms can choose which MLS or portal their listings go to, allowing them to carve out new paths for where listings go. The default appears to still be broad distribution, but the subtext is clearly that they are preparing for a time when that won’t be the case.

Portal preference, MLS mates

Another major wrinkle is that both MLSs and brokerages have started to send exclusive listings directly to portals through partnerships that incentivize agents, brokers and sellers to use pre-marketing. Policy or business disputes also mean that some brokerages and MLSs are trying to cut specific portals off from listings entirely.

MRED briefly pulled its listings from Zillow based on a dispute over IDX filtering rules, while Compass—which has lobbied behind the scenes for these rule changes—also cut Zillow off directly from its own brokerage feeds.

At the same time, Redfin is receiving exclusive Compass listings, and Zillow and other portals also get certain listings from various brokerages.

That opens up the possibility of portals stepping into the flow of listings before wider distribution, instead of brokerages. Notably, these companies seem ready to argue that their platforms, seen by hundreds of millions of consumers, are essentially providing maximum visibility, meaning MLSs are not necessarily required to comply with new state laws.

Again, Compass is pushing the boundary here, with CEO Robert Reffkin promising to get involved if MLSs fine agents who put listings on Redfin, challenging one MLS leader in particular over the idea that properties on that portal weren’t receiving full exposure.

Zillow, on the other hand, has promised its pre-marketing is “designed to work within the MLS framework,” but also claimed that it is bringing pre-market listings “into the light” as the platform with the most visibility for consumers.

While nearly every player has other reasons or motivations for its moves, again the priority is listings. Portals generate revenue from ads and lead sales through listings, and brokerages need listings to attract both agents and clients. As the flow of listings is disrupted, these entities are highly motivated to ensure they are still in the chain—or even carve out their own cache.

‘Outrun extinction’

MLSs are clearly seeing the implications of these moves. While the responses have been varied, the goal appears to be the same—make sure your platform is receiving listings.

Multiple MLSs have launched national membership options—many with the support of Compass, which has subsidized subscriptions by its own agents, provided its listings and offered to support those MLSs in exchange for “enforcing” certain rules. Other MLSs have updated their pre-market policies separately, or consolidated.

In a recent interview with RISMedia, Bright MLS executives said explicitly their priority is ensuring that listings remain available to their subscribers. The MLS—one of a handful that partnered with Compass and opened up its platform—is also working on more “flexibility” that could allow sellers to choose exactly where their listings go.

Bright CEO Brian Donnellan, who previously wrote in an op-ed that MLSs need to “outrun extinction,” told RISMedia that he no longer believes that the industry is going back to the way it was before, with an emphasis on broad exposure for all listings. He envisioned a handful of entities with different exclusive listings—a scenario that would still allow for transparency, he argued.

What is the role of the MLS, if not the first step for listings? Supporters have pointed out that MLSs are a more reliable, consistent source of information about properties—both at the individual and aggregate level—because they are governed by cooperative rulemaking. Everyone should be invested in maintaining that standard, as inconsistent, inaccurate or fragmented information makes it harder for everyone to serve clients.

But with more listings flowing elsewhere, drawn by powerful interests and chasing the allure of removing “negative insights” or boosted exposure on certain portals, a lot of MLSs are recognizing that they need to do more. Donnellan said Bright has to compete in a way it hasn’t before, with technology, support, analytics and price.

Canopy MLS in the Carolinas is also expanding nationally, and CEO Anne Marie DeCatsye told RISMedia that it doesn’t “make sense” for MLSs to operate only regionally when brokerages sprawl across the entire country (or most of it).

That doesn’t really answer the question of where MLSs will fit in the new flow of listings. Donnellan argued that giving brokers control of data is something MLSs can offer, ensuring that outsiders can’t profit or utilize all that data for their own benefit.

The National Association of Realtors® and the Council of Multiple Listing Services recently lobbied federal regulators on the importance of MLSs in ensuring “the largest brokers, portals, or technology companies” don’t dominate real estate.

Hoby Hanna, CEO of Howard Hanna, recently told RISMedia that MLSs used to have “a basic B2B premise,” but became rulemakers instead. He offered a somewhat different vision of the future—with MLSs as “support between one broker and another,” rather than a competitor with the portals, or the arbiter of data use.

One of the MLSs currently operating independently as a non-profit broker cooperative is Northwest Multiple Listing Service (NWMLS) in Washington. It has the opportunity to draw a line in the sand in a legal battle with Compass over rules restricting private listings, giving supporters of “mandatory submission” a road map to maintaining those principles and upholding the original role of the MLS.

At the same, another legal battle between Zillow and MRED in Chicago could also set a precedent—practically or legally—for MLSs who seek to evolve how their data feeds are used, and re-work or revoke IDX license agreements as they pursue a new role in the industry.

{kind=link}